Ready to download as PDF? Use your browser's Print function (Ctrl+P / Cmd+P) and select "Save as PDF" to create a PDF version of this guide.

The Owner's Tax-Smart Investing Playbook

Preserving the Value of Your Success for Generations

How to Build Multi-Generational Wealth by Beating Tax Drag

2026 Edition | Anton Ivanov, iAssure Inc.

How to Benefit From This Playbook

This playbook is not something to skim. It's designed to be read with intention, applied with discipline, and revisited as your circumstances evolve.

Think in decades, not quarters. The strategies here compound over time. Small changes, applied consistently, multiply outcomes. But information without action erodes identity. Understanding these concepts matters less than implementing them.

Systems Over Tactics

This guide focuses on installing systems so the right things happen consistently. It's not about finding the perfect investment or timing the market. It's about building a structure that works regardless of market conditions or tax rule changes.

When you clarify purpose, you make better decisions. These decisions harden into habits, and those habits eventually define your outcomes. The steps in this guide are mechanical. They are small. But small changes, applied consistently over decades, multiply outcomes.

Reading Without Implementation Changes Nothing

Each chapter builds on the previous one. The order matters. Read through once to understand the framework. Then work through the Implementation Checklist with your professional team. The cost of waiting is high. Every year that passes is another year of unnecessary tax drag and lost compounding, a permanent loss of potential wealth.

- Read through once to understand the framework

- Work with your CPA to assess your current structure

- Implement changes systematically, starting with structure

- Review annually with your professional team

- Return to specific chapters as your situation evolves

This playbook is designed for business owners with $500,000+ in retained earnings or $50,000+ in annual passive income who are thinking in decades. It is likely less useful for early-stage founders requiring all capital for operations or those focused primarily on short-term cash flow management.

I am not a tax lawyer, not an accountant, not a lawyer. This guide does not constitute advice. Advice on investments and insurance is provided after a formal engagement and after knowing your situation. All topics must be taken as ideas for conversations you might want to have with your tax advisor, investment advisor, and your insurance advisor.

Table of Contents

- How to Benefit From This Playbook

- PART I: HOW DYNASTY THINKERS SEE THE WORLD

- 1. Why This Matters More Than Ever

- 2. The Dynasty Lens: From Corporation to System

- PART II: STRUCTURE FIRST

- 3. Structure Before Strategy

- 4. Purpose Determines Risk & Extraction Strategies

- PART III: THE TAX MECHANICS ENGINE

- 5. The True Cost of Passive Income Tax

- 6. The Power of Capital Gains

- 7. The $50,000 Passive Income Threshold

- 8. Asset Location: Where to Hold What

- 9. The Other Half of the Equation: Investment Selection

- PART IV: FLOW DESIGN

- 10. RDTOH & GRIP: Unlocking Trapped Capital

- 11. The Capital Dividend Account

- 12. Corporate Class Funds & Strategic Withdrawals

- 13. Borrowing to Invest

- PART V: INSURANCE AS A BALANCE-SHEET ASSET

- 14. The Foundation: Access to Top-Tier Insurance Products

- 15. Advanced Life Insurance-Based Planning

- 16. The Tax-Sheltered Universe

- PART VI: RETIREMENT, ESTATE, CONTINUITY

- 17. Retirement as Multi-Decade Wealth Transfer

- 18. Estate Strategies: Passing Wealth Forward

- PART VII: INTEGRATION & ACTION

- 19. The Dynasty Flow of Funds: Where the Next Dollar Goes

- 20. Coordination: Working With Your Professional Team

- 21. Implementation Checklist & Next Steps

PART I: HOW DYNASTY THINKERS SEE THE WORLD

1. Why This Matters More Than Ever

As a business owner, you're an expert at generating returns. But in Canada, the return you earn and the return you keep can be vastly different. For investments held inside your corporation, tax drag, the slow, silent erosion of wealth from annual taxes on passive income, is often the single biggest obstacle to building a lasting legacy.

While getting the extra 1% in market returns is important, and while at iAssure working with recognized fund managers proven to deliver consistent value is non-negotiable, these efforts are dwarfed by the power of tax structure and strategy. The difference between a standard corporate investment portfolio and a tax-optimized one can be hundreds of thousands, or even millions, of dollars over your lifetime.

Developments for 2026 and Beyond

CRA Doesn't Want You to Eat Your Cake

Over the past two decades, Canadian corporate tax rates have stabilized or improved. The federal general rate has been steady at 15% since 2012, and the small business rate dropped to 9% by 2019, making it advantageous to retain and reinvest earnings inside your company. Yet pulling those profits out for personal use has become far more expensive, with top personal combined marginal rates now exceeding 53% in Ontario and Quebec. Escalating fiscal deficits only heighten the risk of future tax pressures, further penalizing extraction. You are rich until you try to cash out.

Call It Inflation or Dollar Devaluation: If You Keep Cash, You Lose Value

Amid rising risks of persistent inflation and currency devaluation fueled by quantitative easing's money-printing effects, suspected Trump policies favoring dollar weakening, China's aggressive gold and silver accumulation (echoed by other governments) pressuring the USD, and the Yen carry trade, all eroding the value of the USD and CAD (given their close ties), as well as trade tensions and tariffs, shrinking capital investment undermining competitiveness, and weakening labor markets impacting revenue streams, holding idle cash in your corp or personally means watching its purchasing power diminish steadily. Anything that equates to cash like GICs, bonds, bond funds, the fixed income portion of balanced funds, even inflation-indexed bonds (basically most asset classes considered conservative, safe) are becoming purchasing power melting pots. Just see what gold and silver did in 2025.

Market Volatility Is Increasing Systematically

Disorderly market sell-offs are becoming more frequent, threatening portfolio values within your investments or corp holdings, amplified by algorithmic trading that reacts in milliseconds to news, the surge in ETFs causing herd-like movements in asset prices, heavy concentration in major indexes (e.g., dominated by a handful of tech giants), and the rise of 0DTE (zero days to expiration) options trading, which injects short-term speculation and exacerbates daily swings. This heightened volatility demands vigilance, as it can erode gains faster than ever, even in a broadly rising market.

This all underscores the even more critical importance of:

- A laser-sharp focus on optimizing the growth of your portfolio by accounting for the bottom line: what you and your family get after money is extracted out of the corporation and all taxes have been paid.

- A systematic long-term extraction strategy, prioritizing what truly matters: returning ownership of your money to you by minimizing the taxman's share.

- A long-term asset growth and protection framework for the money that is to be left in the corp considering an even higher concentration of risk.

This guide will walk you through the core strategies used by Canada's more successful families to protect and compound their corporate wealth. It's designed to shift your focus from simply earning returns to building a powerful, tax-efficient engine for multi-generational success.

Thinking in Decades, Not Quarters

When you think like a dynasty, you ask different questions:

- How does this decision affect outcomes over 20 years?

- What will this structure allow us to do in 10 years that we can't do today?

- How do we pass wealth to the next generation efficiently?

- What systems do we install so the right things happen consistently?

This mindset shift changes everything. It moves you from reactive annual filing to proactive wealth preservation. From annual optimization to generational thinking.

2. The Dynasty Lens: From Corporation to System

This is one of the most important distinctions in dynasty planning: Dynasty builders do not think in terms of "my corporation" as a single object. They think in systems.

Operating entities come and go. Capital structures persist. The purpose of planning is not to empty the HoldCo efficiently, but to decide what stays, what flows, and when.

Dynasty thinking is not about keeping wealth locked inside a corporation forever. It is about deciding which container compounds, which container distributes, and which container eventually dissolves, on purpose.

The Three Layers of Dynasty Thinking

Right now, many guides treat "the corporation" as a single object. That's where confusion comes from. A dynasty builder thinks in layers, not entities.

Layer 1: Operating Layer (Transitional by Nature)

Operating Companies (OpCos) are tools. They exist to:

- Generate active income

- Take risk

- Be sold, merged, wound down, or replaced

They are expected to change. No dynasty assumes the same operating entity survives generations unchanged.

OpCos are explicitly transitional.

Layer 2: Capital Stewardship Layer (Semi-Permanent)

Holding Companies (HoldCos) are continuity vehicles. They exist to:

- Store accumulated capital

- Separate risk from assets

- Preserve optionality

- Serve as the family's long-term balance sheet

A HoldCo may evolve legally, but its function persists. This is where dynasty thinking actually lives.

HoldCos are capital stewardship vehicles designed to endure across decades, and sometimes generations.

Layer 3: Beneficiary Layer (Eventual Destination)

Individuals, trusts, and estates are the final recipients, but not necessarily the primary compounding engines.

Extraction happens:

- Gradually for lifestyle

- Strategically for planning

- Heavily at death (where efficiency is highest)

Extraction is planned, not avoided.

The Three Extraction Flows

A dynasty builder optimizes when tax is paid, not whether it is paid. Extraction happens in three distinct flows:

1. Lifestyle Flow (Inevitable, Taxable)

- Salaries and dividends for living

- Managed to stay within optimal brackets

- Accepted as a cost of consumption

This is not failure. It's maintenance.

2. Planning Flow (Optimized, Structured)

- CDA dividends (tax-free extraction)

- Capital gains planning

- RRSP/TFSA/IPPs

- Debt reduction

This is systematic leakage control, not extraction.

3. Estate Flow (Highest Efficiency)

- Corporate-owned life insurance

- CDA at death

- Estate freezes

- Trust distributions

This is where maximum efficiency occurs.

The Three-Layer Tax Challenge

When extraction is needed, corporate wealth faces multiple tax events:

- Corporate level: Tax on investment income as it's earned

- Personal level: Tax when dividends or salary are paid

- Estate level: Tax on remaining corporate assets at death

The goal is to minimize extraction (keep wealth in HoldCo) and maximize tax efficiency when extraction is necessary.

Planning for Dynasty

When evaluating any strategy, ask:

- Does this keep wealth in the HoldCo for generations?

- When extraction is needed, what's the most tax-efficient method?

- How can we use CDA, life insurance, and estate opportunities to extract efficiently?

- What's the minimum extraction needed for lifestyle and personal asset building?

If you can't answer these questions, you're optimizing in isolation. The most efficient corporate strategy is less valuable if it traps wealth or creates significant extraction costs.

Think of your OpCo as transitional, it may be sold or wound down. Think of your HoldCo as the permanent dynasty vehicle, where accumulated wealth compounds for generations. Extraction is systematic, minimal, and always tax-efficient. It's not a plan to empty the HoldCo, but a plan to sustain lifestyle while preserving the dynasty vehicle.

PART II: STRUCTURE FIRST

3. Structure Before Strategy

Before we discuss returns or managers, we address structure. Structure determines what is possible. It determines what options remain available to you ten years from now.

Why Structure Matters

Structure creates optionality. The right structure today allows you to make better decisions tomorrow. A structure that doesn't align with your goals limits your options and can create costly problems later.

The HoldCo: Safety and Purity

Separating operating risk from accumulated capital is foundational. When operating assets and investment assets are mixed in one corporation, a lawsuit or liability in the business can threaten your life's savings.

A Holding Company (HoldCo) creates a legal barrier. Beyond safety, it helps preserve eligibility for the Lifetime Capital Gains Exemption (LCGE), which was increased to $1.25 million in 2024.

If your operating company holds too much "passive" investment capital, you may disqualify yourself from this substantial tax-free benefit upon sale.

When to Consider a HoldCo

How HoldCo Works

A typical structure:

- Operating Company (OpCo): Runs the business, earns active income

- Holding Company (HoldCo): Holds investments, receives dividends from OpCo

- Personal: Receives dividends or salary from OpCo or HoldCo

This separation provides:

- Asset protection: Business liabilities can't reach investment assets

- Tax flexibility: Can move money between entities strategically

- Estate planning: Can transfer ownership of HoldCo separately from OpCo

- Purification: Keeps OpCo "pure" for LCGE eligibility

Example: The Operator vs. The Architect

Two business owners both sell their operating companies for $5 million after 20 years.

Owner A (The Operator): Kept all excess cash inside the operating company.

- Result: The OpCo was "contaminated" with too much passive asset value.

- Consequence: Disqualified from the Lifetime Capital Gains Exemption (LCGE).

- Outcome: Pays capital gains tax on the full $5 million immediately. No structure to manage the after-tax wealth for the next generation.

Owner B (The Architect): Systematically moved excess cash to a HoldCo every year.

- Result: The OpCo remained "pure" (mostly active business assets).

- Consequence: Qualified for the $1.25M+ LCGE (tax-free capital gain).

- Outcome: Saves ~$300,000+ in immediate tax. The sale proceeds flow into the HoldCo, which now serves as the family's long-term investment engine, separate from the risk of the previous business.

The Difference: The Architect didn't just build a business; they built a system to capture and keep the value of that business.

Trusts: Flexible Distribution

Where appropriate, trusts introduce optionality. While they add complexity, they allow a founder to maintain control over assets while gradually transferring economic benefit to beneficiaries who may be in lower tax brackets.

This is crucial for managing tax across a family unit. Income can be distributed to family members in lower tax brackets, reducing total family tax.

Trust structures require legal and tax advice. They add complexity and ongoing costs. Only use them when the benefits clearly outweigh the costs. Always work with your lawyer and CPA before implementing trust structures.

Structure comes before strategy. Get the structure right, and your investment decisions become simpler. Without the right structure, you may spend years working around limitations you could have avoided.

4. Purpose Determines Risk & Extraction Strategies

A corporate portfolio is rarely just "one thing." Usually, it's a mix of capital with different jobs. Clarity on how the "cake" is divided helps prevent accidental risk. But purpose also determines extraction strategy. The earlier extraction strategies are set in place, the more effective they are in minimizing tax.

The Three Buckets

Divide your corporate capital into three buckets:

Bucket 1: Near-Term Business Capital (3-5 years)

- Purpose: Business opportunities, working capital buffer

- Risk tolerance: Low to moderate

- Liquidity: High

- Tax strategy: Preserve capital, minimize tax events

- Extraction planning: Likely minimal extraction needed; focus on maintaining capital for business use

Bucket 2: Retirement Capital (10+ years)

- Purpose: Your personal retirement

- Risk tolerance: Moderate to high

- Liquidity: Lower priority

- Tax strategy: Tax-efficient growth, deferral

- Extraction planning: Lifestyle extraction flow; plan for systematic, tax-efficient withdrawals during retirement years

Bucket 3: Legacy Capital (20+ years)

- Purpose: Estate transfer to next generation

- Risk tolerance: Can be higher

- Liquidity: Not required until transfer

- Tax strategy: Long-term tax efficiency, estate structures

- Extraction planning: Estate extraction flow; maximize tax-efficient extraction at death through life insurance and CDA

Legacy capital is often intentionally not meant to be extracted during the founder's lifetime. Its purpose is continuity, not consumption. This capital stays in the HoldCo to compound for generations.

Why This Matters

Without clarity on purpose, you might:

- Expose short-term business funds to market volatility

- Leave long-term legacy funds sitting in low-yield cash

- Make investment decisions without understanding the time horizon

- Choose risk levels that don't match the capital's job

- Fail to plan extraction strategies early, missing opportunities for tax efficiency

Clarity simplifies decisions. If you know that $500,000 is intended for estate transfer, that portion can be structured differently, perhaps utilizing permanent insurance or long-term growth assets, compared to capital you plan to extract next year.

The Two Extraction Flows

Extraction planning requires managing two distinct flows, each with different strategies and timing:

1. Lifestyle Extraction Flow (You Need This)

This is the extraction you need for personal consumption and lifestyle support. It happens during your lifetime and must be planned systematically to minimize tax drag.

Strategies for lifestyle extraction include:

- CDA dividends: Tax-free extraction when CDA balance is available

- Strategic dividend timing: Coordinate with RDTOH recovery and personal tax brackets

- Preferred share redemption: From estate freeze structures, providing tax-efficient capital extraction

- Split dollar strategies: With corporate-owned life insurance, allowing tax-efficient access to policy cash value

- Capital gains realization: When strategically timed to optimize tax brackets

- RRSP/TFSA contributions: Using extracted funds to build personal registered accounts

The earlier you establish these extraction mechanisms, the more effective they become. Setting up an estate freeze early creates preferred shares that can be redeemed tax-efficiently later. Establishing corporate-owned life insurance early builds cash value and CDA credits that become available when needed.

2. Estate Extraction Flow (You Want to Maximize This)

This is the extraction that happens at death, where tax efficiency is highest. This is where you want to maximize extraction because the tax treatment is most favorable.

Strategies for estate extraction include:

- Corporate-owned life insurance: Death benefit creates CDA credit for tax-free distribution to beneficiaries

- CDA at death: Capital gains realized at death create CDA, allowing tax-free distribution

- Estate freeze benefits: Future growth transferred to next generation at lower tax cost

- Trust distributions: Tax-efficient transfer to beneficiaries

This is why extraction strategies at death has such importance and should be planned as early as possible. Corporate-owned life insurance requires time to build value and requires underwriting while you're healthy. Estate freezes work best when implemented early, before significant growth occurs. The earlier you establish these structures, the more tax-efficient your estate extraction becomes.

Extraction strategies are most effective when established early. A life insurance policy purchased at age 45 has 30+ years to build cash value and CDA credits. An estate freeze implemented before significant growth occurs transfers more value tax-efficiently. Preferred shares created through an estate freeze can be redeemed strategically over decades. The earlier extraction strategies begins, the more options you have and the more tax-efficient the outcomes.

Defining Your Buckets and Extraction Strategy

Purpose determines risk. When you know what each dollar is for, investment decisions become simpler and more effective. Clarity on purpose prevents accidental risk and ensures each portion of your portfolio is doing its job. But purpose also determines extraction strategy. Plan extraction early: lifestyle extraction for what you need during your lifetime, and estate extraction for what you want to maximize at death. The earlier extraction strategies are established, the more tax-efficient they become.

PART III: THE TAX MECHANICS ENGINE

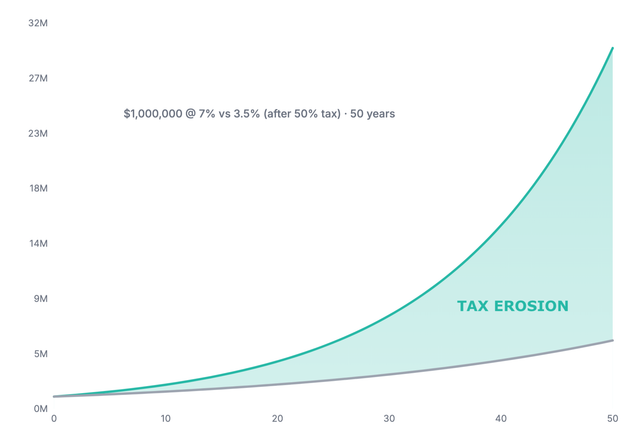

5. The True Cost of Passive Income Tax

Most business owners understand compounding: your returns earn returns, and wealth grows exponentially. The problem is that taxes also compound, against you. Passive investment income earned inside a Canadian corporation can be taxed at rates around 50%. This annual tax drag acts like a powerful brake on your wealth-building engine.

Let's compare two scenarios for a corporation investing $1,000,000 over the long term, both earning a 7% gross return.

- Scenario A: Invested in a standard portfolio, paying ~50% tax on passive income annually.

- Scenario B: Invested in a tax-optimized structure that defers and minimizes tax.

Source: iAssure Inc. | Tax erosion comparison over 50 years

The difference is substantial. This gap doesn't come from taking more risk or "beating the market." It comes from managing tax efficiency.

What This Graph Shows:

The chart above illustrates the erosion of wealth inside a corporation over 50 years.

- Scenario A (Tax Drag): Invested in interest-bearing assets (taxed at ~50% annually). The growth curve is flattened significantly because half the return is lost every year.

- Scenario B (Tax Efficient): Invested in deferred capital gains. The curve stays steeper because tax is deferred until the end.

The Real-World Impact (Net to You):

It's not just about the corporate account balance; it's about what you keep. If we start with $1,000,000 at a 7% return:

- Inefficient Path: After 50 years, the corporation holds ~$5.5 million. After extraction taxes, you keep approximately $4.1 million.

- Efficient Path: After 50 years, the corporation holds ~$29.4 million. Even after paying the deferred capital gains tax and extraction taxes, you keep approximately $18.5 million.

The Difference: $14 Million+ in additional family wealth, simply by choosing the efficient path. This illustrates the massive long-term value of optimizing your corporate investment assets for tax efficiency.

For long-term corporate investing, tax friction is often the primary headwind. Managing tax efficiency often yields more reliable outcomes than stock selection.

6. The Power of Capital Gains

Not all investment income is created equal. Inside a corporation, the type of income you earn has a significant impact on how much you keep.

- Interest Income: Taxed at the highest rate, ~50%. You keep about $50 of every $100.

- Capital Gains: Taxed at the most favorable rate, ~25%. You keep about $75 of every $100, and the other non-taxable portion can be paid out of the corporation tax-free via the Capital Dividend Account (CDA).

The goal is simple: design your corporate investment portfolio to minimize annual interest and dividend income and maximize strategically realized capital gains.

This is achieved through:

- Growth-focused equity investments.

- Corporate class funds designed for tax efficiency.

- A disciplined buy-and-hold approach that defers tax realization for years, or even decades, allowing your full pre-tax capital to compound for as long as possible.

Capital Gains in 2026 and Beyond

For years, capital gains were the undisputed driver of corporate investment efficiency. Historically, only 50% of a realized gain was taxable.

As of 2026, the capital gains inclusion rate for corporations remains at 50%. The proposed increase to 66.67% from the 2024 federal budget was cancelled in March 2025. While the rate is stable for now, tax rules change over time, and building tax-efficient structures today provides resilience regardless of future policy direction.

This does not mean we stop investing. It means we consider timing more carefully, specifically when we choose to realize gains, and we use structures that allow tax deferral more strategically.

Impact on Strategy

The government's intent to potentially increase the inclusion rate affects several areas:

- Realization Timing: With potential higher tax on realized gains in the future, deferral becomes even more valuable

- Portfolio Structure: Capital gains remain more efficient than interest income, making growth-focused strategies important

- Estate Strategies: For estate transfer, tax-efficient structures (like corporate-owned life insurance) become relatively more attractive

Example: The High Cost of Inefficiency

Consider two corporations, each with a $2,000,000 portfolio earning 7% annually ($140,000/year).

Scenario A: The "Passive" Approach (Interest Heavy)

- Income: Earns mostly interest income (taxed at ~50.17%).

- Tax Bill: ~$70,238 annually.

- Net Growth: Only $69,762 is left to compound.

- Result: The portfolio grows at roughly 3.5% after tax. Wealth doubles every 20 years.

Scenario B: The "Dynasty" Approach (Capital Gains Focus)

- Income: Earns mostly deferred capital gains.

- Tax Bill: $0 annually (until sold).

- Net Growth: The full $140,000 stays in the account to compound.

- Result: The portfolio grows at 7% pre-tax. Wealth doubles every 10 years.

The 20-Year Difference:

- Scenario A grows to: ~$3.9 Million

- Scenario B grows to: ~$7.7 Million (Pre-liquidation tax)

Even after paying tax on the final sale in Scenario B, the "Dynasty" approach results in significantly more after-tax wealth for the family, purely due to structural efficiency.

Note: This example is illustrative only. Assumptions: 7% annual return, 50.17% corporate tax rate on interest income. Scenario B assumes deferred capital gains with no annual turnover for illustration purposes. Actual results depend on your specific tax rates and investment selection.If you're considering realizing capital gains, discuss timing with your CPA. There may be strategic reasons to defer gains further or to use tax-efficient structures. Every situation is unique. The government's intent suggests that tax-efficient planning will become increasingly important.

In corporate investing, it's not just what you earn, it's how you earn it. Shifting your returns toward capital gains is one of the most powerful levers you can pull. With the inclusion rate at 50%, capital gains remain the most tax-efficient form of corporate investment income. Building tax-efficient structures today provides resilience regardless of future policy changes.

7. The $50,000 Passive Income Threshold

Important Note: This threshold applies only to businesses that are still eligible for the small business tax rate. If your corporation has already lost its small business deduction or is taxed at the general rate, this threshold does not apply.

When your corporation earns more than $50,000 in passive investment income in a single year, your Small Business Deduction (SBD) begins to shrink. This creates a "tax drag" on your active business income.

How the SBD Grind Works

The mechanism:

- For every $1 of passive income above $50,000, you lose $5 of small business deduction

- At $150,000 of passive income, the SBD is eliminated entirely

- This can increase your corporate tax rate from ~12-15% (small business rate) to ~26-27% (general rate) on active business income

This isn't just about investment income tax. It's about the tax rate on your operating business. Passive investment income can increase the tax rate on active business income.

What Counts as Passive Income

What counts:

- Interest income

- Foreign dividends

- Rental income (from passive properties)

- Taxable capital gains (realized)

- Certain other passive income types

What does NOT count:

- Unrealized capital gains (until sold)

- Income from an IPP

- Growth inside a permanent life insurance policy

- Return of capital distributions (ROC)

Managing the Threshold

Strategies to manage passive income:

- Focus on Unrealized Gains: Hold investments that appreciate in value but don't generate annual income

- Use Corporate Class Funds: Minimize annual interest and foreign dividend distributions

- Consider Life Insurance: Growth inside a permanent life insurance policy doesn't count toward passive income

- Use Individual Pension Plans (IPP): Income inside an IPP doesn't count toward the $50,000 threshold

Monitoring Your Passive Income

The $50,000 threshold is a constraint to manage, not a barrier to avoid. Understanding it helps you make informed decisions about portfolio structure. Work with your CPA to monitor and manage your passive income level.

8. Asset Location: Where to Hold What

This is one of the more immediate and actionable levers for most business owners. Because tax rates differ wildly between your corporation and your personal accounts, where you hold an asset matters as much as what you buy.

The Basic Principle

Inside a corporation, "passive" income (interest and foreign dividends) is punished with the highest immediate tax rates. Therefore, we want to evict these assets from the corporate balance sheet whenever possible.

The Ideal Split

1. In the Corporation (Prioritize Capital Gains)

With the 50% inclusion rate, capital gains remain the most efficient form of taxable corporate income. Focus your corporate portfolio on assets that generate growth (stocks, equity funds, real estate) rather than yield. We want to defer the tax event as long as possible to let the capital compound.

2. In Personal Registered Accounts (Prioritize Yield)

Your RRSP and TFSA are the perfect homes for investments that generate interest, bonds, or high dividends. Since these accounts are tax-sheltered (or tax-deferred), the high tax rate that would apply to interest income is neutralized. Use your personal room to hold the "heavy tax" assets.

3. In Corporate Life Insurance (The Ultimate Shelter)

If you have exhausted your personal registered room and still have fixed-income or conservative capital to invest, consider permanent life insurance. It acts as a tax-exempt shelter for what would otherwise be highly taxed conservative growth.

Example: Asset Location Strategy

Scenario: You have $1,000,000 to invest, split between corporate and personal accounts.

Corporate account ($600,000): Invest in growth-oriented equity funds that generate capital gains (unrealized until sold). This defers tax and keeps passive income low.

Personal RRSP ($300,000): Invest in bonds and fixed-income that generate interest. The RRSP shelters this from immediate tax.

Personal TFSA ($100,000): Invest in any asset class. Growth is tax-free.

Result: Interest income is sheltered in registered accounts. Capital gains are deferred in the corporation. Total tax drag is minimized.

Note: This example is illustrative only. Actual allocation depends on your specific circumstances, registered account room, and investment goals.Asset location is one of the most powerful tax optimization tools available. Where you hold an asset can matter more than which asset you choose. Review your asset location annually and adjust as your circumstances change.

9. The Other Half of the Equation: Investment Selection

Tax optimization determines how much of your return you keep. Investment selection determines how much you earn in the first place. A perfect tax strategy with mediocre investments will still produce a mediocre result.

That is why our approach is twofold: we combine advanced tax-efficient structuring with direct access to a curated selection of investment managers recognized by the industry for their proven track record.

For decades, we have analyzed the Canadian investment landscape, focusing on after-fee, risk-adjusted performance across full market cycles. Our clients benefit from portfolios built with managers who have proven to deliver net results, providing the powerful engine of growth that our tax strategies then protect.

When you pair proven investment management with tax strategy, you create a compounding advantage that is nearly impossible to replicate.

PART IV: FLOW DESIGN

10. RDTOH & GRIP: Unlocking Trapped Capital

In Canada, we have an "integrated" tax system designed to ensure total taxes remain roughly the same whether earned personally or through a corporation. RDTOH and GRIP are the mechanisms that make this work.

However, understanding them is not just about compliance. It is about liquidity.

When your corporation earns passive income, the CRA takes a massive upfront portion, roughly 50%. A significant chunk of this (30–38%) is "refundable," but only if you take specific actions.

The "Interest-Free Loan" Trap

If you do not trigger these refunds annually, roughly one-third of your investment income sits with the CRA as an interest-free loan. This is trapped capital. It sits idle in a government account instead of compounding in your portfolio.

Over ten or twenty years, the difference between reinvesting that 30% refund annually versus leaving it trapped is massive.

RDTOH: Refundable Dividend Tax on Hand

RDTOH is a notional account that tracks the refundable taxes your corporation has paid on passive income.

Note: Since 2019, this is tracked in two accounts: Eligible RDTOH (ERDTOH) and Non-Eligible RDTOH (NERDTOH).

The Mechanism:

- High Upfront Tax: Your corporation earns passive income (like interest or rent) and pays ~50% tax immediately.

- The "Deposit": A large portion (30.67% for interest, 38.33% for portfolio dividends) is added to your RDTOH balance. This is the "loan" you have made to the CRA.

- The Refund Trigger: When the corporation pays taxable dividends to shareholders, the CRA refunds this tax to the corporation.

The Trap:

To recover taxes on interest income (NERDTOH), you generally must pay non-eligible dividends. If you only pay eligible dividends (to save personal tax), the refund may remain trapped, and your corporate capital base shrinks.

GRIP: General Rate Income Pool

GRIP tracks active business income that was taxed at the higher general corporate rate. It allows you to pay Eligible Dividends, which are taxed at a lower personal rate for you.

The Balancing Act:

The goal is to stop the "leakage." You want to pay just enough dividends to recover your RDTOH (getting your cash back from the CRA) while using GRIP to minimize the personal tax on those dividends.

Example: The Cost of Trapped Capital

Scenario: Your corporation earns $10,000 of interest income.

- Corporate Tax Paid: ~$5,000 (Immediate cash outflow).

- Refundable Portion: ~$3,067 is tracked in NERDTOH.

Scenario A: The "Passive" Approach (Trapped Capital)

You decide not to pay a dividend this year.

- Result: The $3,067 stays with the CRA. You have lost the ability to reinvest that capital. It generates zero return for you.

Scenario B: The "Optimized" Approach (Compounding Capital)

You declare a non-eligible dividend of ~$8,000 to yourself.

- Result: The corporation receives the $3,067 refund.

- Impact: That $3,067 is now back in your hands (or the corporation's hands, effectively) to be deployed. Instead of an interest-free loan to the government, it becomes fuel for your next investment.

This example is illustrative only and not a substitute for professional advice. Assumptions: 50% corporate tax rate on passive income, 30.67% refundable portion for interest income. Actual rates vary by province and circumstances. Consult your CPA for calculations specific to your situation.

Don't view RDTOH as just accounting. View it as capital efficiency. Every dollar of RDTOH left in the corporation is a dollar that isn't working for your dynasty. Work with your CPA to ensure you are clearing these refundable balances annually so your capital compounds for you, not the CRA.

- "Do we have a balance in our NERDTOH (Non-Eligible) account that is currently trapped?"

- "Are we paying enough non-eligible dividends to recover our refundable taxes every year?"

- "Is our dividend strategy optimizing for Net Cash in Hand (recovering corporate refunds) or just minimizing personal tax rates?"

11. The Capital Dividend Account

The Capital Dividend Account (CDA) is a notional account that tracks tax-free amounts available to a Canadian-controlled private corporation (CCPC) to pay as capital dividends to shareholders.

Capital dividends are a special type of dividend that is received tax-free by shareholders. This makes the CDA one of the most powerful tax-sheltering tools for Canadian corporations.

How the CDA Works

The CDA increases when your corporation:

- Realizes capital gains: With the 50% inclusion rate, 50% of the gain is added to the CDA (representing the non-taxable portion).

- Receives life insurance proceeds: The amount (net of adjusted cost base) is added to the CDA

When capital dividends are paid from the CDA, they are received tax-free by shareholders. This allows you to extract corporate wealth without personal tax.

Example: CDA in Action

Year 1: Building the CDA (2026 Rules)

- Corporation sells investments: Cost $1,500,000, Proceeds $2,000,000

- Capital gain: $500,000

- CDA addition: $250,000 (50% of $500,000, representing the non-taxable portion under the 50% inclusion rate)

- CDA balance: $250,000

Year 2: Receiving Life Insurance Proceeds

- Life insurance proceeds received: $1,000,000

- Adjusted cost base: $50,000 (simplified for illustration; actual ACB = premiums paid minus net cost of pure insurance (NCPI), which increases with the insured's age. For older policies, ACB may be significantly lower or even zero)

- CDA addition: $950,000

- CDA balance: $1,200,000

Year 3: Using the CDA (Estate/Beneficiaries)

- CDA balance: $1,200,000

- Beneficiaries want to extract: $800,000 for estate distribution

- Capital dividend paid: $800,000

- CDA balance after: $400,000

- Tax impact: $800,000 received tax-free by beneficiaries

- Comparison: If this were a regular dividend, the beneficiaries would pay significant personal tax (potentially $200,000+ depending on province and other income)

The CDA provides a tax-free extraction mechanism that can significantly enhance after-tax wealth. It's particularly powerful when combined with capital gains and corporate-owned life insurance. Work with your CPA to understand how the CDA applies to your situation.

- What is our current CDA balance?

- How are we tracking capital gains for CDA purposes?

- Are we coordinating dividend payments with our CDA balance?

- How does our life insurance strategy contribute to CDA building?

12. Corporate Class Funds & Strategic Withdrawals

Corporate class mutual funds remain a highly effective tool for tax optimization. Their unique structure allows them to minimize annual taxable distributions and emphasize tax-efficient capital gains over heavily taxed interest and dividends.

In a traditional mutual fund, all income (interest, dividends, gains) flows through to you annually, creating tax drag. Corporate class funds, however, can often recharacterize income and minimize payouts, keeping more of your money compounding. When paired with T-series funds, they become even more powerful. T-series funds favor the distribution of capital in early years, deferring taxes by deferring the distribution of gains.

Corporate class funds are a powerful tool for managing the type and timing of taxable income, reducing annual tax drag, and preserving the power of compounding.

13. Borrowing to Invest

For corporations, borrowing to invest isn't speculation; it's a disciplined, tax-smart strategy. When your corporation borrows to earn investment income, the interest expense is generally tax-deductible. This lowers your taxable passive income, reducing tax drag and allowing more of your capital to compound.

The wealthiest individuals and corporations use this principle constantly: they use Other People's Money (OPM) to grow faster. Even if your investment return merely equals your borrowing cost, you can still come out ahead due to the tax savings and the fact that your returns compound on a growing asset base while your loan cost remains fixed.

Important considerations: Leverage comes with risks related to the stability of the cash flow required for interest payments and to interest rates. It also increases your exposure to market risks. Borrowing to invest should only be considered when you have stable cash flow to service the debt and can tolerate the additional market risk.

While the math often favors leverage, the peace of mind of a debt-free balance sheet has its own value. This strategy is for those who view debt as a tool, not a burden. The emotional cost of carrying debt should factor into your decision alongside the mathematical benefits.

Example: Borrowing to Invest

Let's compare investing $1M of your own capital versus investing your $1M plus $300k borrowed at a low, secured rate over 25 years. Assumptions: 6% gross annual return, 50% tax rate on investment income, 4% interest rate on loan, interest-only loan structure.

Scenario A: No Leverage

- Initial investment: $1,000,000

- After-tax return: 3% (6% gross with 50% tax drag)

- After 25 years: approximately $2,093,000

Scenario B: With Leverage

- Initial investment: $1,300,000 ($1M own capital + $300k borrowed)

- After-tax return on investment: 3% (same tax drag applied to investment income)

- Annual interest cost: $12,000 ($300k × 4%)

- Annual tax savings from interest deduction: $6,000 ($12,000 × 50% tax rate)

- Net annual interest cost after tax: $6,000

- Total interest paid over 25 years: $300,000

- Total tax savings over 25 years: $150,000

- Investment value after 25 years: approximately $2,722,000

- Less: Loan principal repayment: $300,000

- Less: Net interest cost (interest paid minus tax savings): $150,000

- Final net balance: approximately $2,272,000

The difference: $179,000 additional wealth ($2,272,000 - $2,093,000) created through strategic leverage, despite the interest costs.

Note: This example is illustrative only. Assumptions: interest-only loan (principal repaid at end), constant 6% return, 50% tax rate, 4% interest rate. Actual results depend on investment performance, interest rates, tax rates, loan terms, and market conditions. Borrowing to invest involves risk and requires careful analysis. Always consult with your CPA and investment advisor before implementing leverage strategies.

Done prudently, borrowing to invest expands your capital base, reduces tax drag through interest deductibility, and accelerates long-term wealth creation.

PART V: INSURANCE AS A BALANCE-SHEET ASSET

14. The Foundation: Access to Top-Tier Insurance Products

Just as not all investment managers are equal, not all insurance products are created equal. The advanced strategies discussed in this guide rely on a high-quality permanent life insurance policy as their foundation. The choice of carrier and product design is critical.

We work directly with Canada's recognized life insurers, companies with strong financial strength, decades of consistent performance in their participating accounts, and product designs suited for corporate applications. We analyze the market to select the right product from the right carrier, ensuring the foundation of your plan is as strong as the strategy itself.

The success of advanced insurance strategies depends entirely on the quality of the underlying policy. Securing the right product from the right carrier is non-negotiable.

15. Advanced Life Insurance-Based Planning

Beyond its basic tax-sheltering function, corporate-owned permanent life insurance can be used in several advanced strategies to unlock capital, finance operations, and maximize estate value.

Insured Retirement Program (IRP)

The corporation builds up tax-sheltered cash value inside a policy. In retirement, this cash value is used as collateral for a series of annually received loans, providing you with tax-free personal cash flow similar to retirement income. The interest and the capital are reimbursed to the lender by the tax-free death benefit, leaving the remainder for your estate.

Corporate Estate Bond

The corporation invests surplus cash into a permanent life policy. The tax-sheltered growth results in a larger after-tax estate value compared to a taxable investment in the earlier years of the strategy and often delivers better results even beyond life expectancy. The death benefit creates a credit to the CDA for tax-free distribution.

Immediate Financing Arrangement (IFA)

A strategy where a corporation buys a large policy and immediately borrows back most of the premium. This unlocks capital for business use while the policy continues its tax-sheltered growth. The interest on the loan may be deductible, and the premium paid might also turn out to be tax deductible. Note: This strategy requires careful structuring and professional advice.

These advanced strategies are complex and require careful structuring. They involve significant policy premiums and ongoing costs. Always work with qualified insurance and tax advisors to understand the risks, costs, and suitability for your situation.

These advanced strategies transform a life insurance policy from a simple protective tool into a dynamic financial instrument for retirement funding, leverage, and unparalleled estate tax efficiency.

16. The Tax-Sheltered Universe

The most powerful way to defeat tax drag is to remove your investments from the passive income regime entirely. Corporate-owned permanent life insurance allows corporate assets to grow tax-sheltered, meaning 100% of your returns stay invested and compound without any annual tax erosion.

Corporate-Owned Permanent Life Insurance

Far more than just insurance, this is a multi-purpose financial tool that serves as the foundation for tax-efficient corporate wealth building.

How it works:

- The policy's internal cash value grows tax-sheltered

- Growth inside the policy doesn't count toward the $50,000 passive income threshold

- The eventual death benefit is paid to the corporation tax-free

- This tax-free amount then creates a credit in the Capital Dividend Account (CDA), which is usually very close to the actual death benefit (though not always at 100%), allowing the wealth to be distributed to your heirs tax-free

- Cash value can be accessed through policy loans or split dollar strategies for lifestyle extraction

Strategic applications:

- Corporate Estate Bond: Building tax-sheltered wealth that creates CDA at death

- Estate liquidity: Providing funds to pay taxes on corporate assets at death

- CDA building: Creating tax-free extraction capacity for beneficiaries

- Passive income management: Moving capital out of the passive income regime

Why it matters:

Corporate-owned life insurance is one of the most powerful tools for dynasty building. It provides tax-sheltered growth, estate liquidity, and CDA credits for tax-free distribution. The earlier you establish these policies, the more value they build and the more tax-efficient your estate extraction becomes.

Individual Pension Plans (IPPs)

An IPP is a corporate-sponsored pension plan for owner-managers. While IPPs can provide higher contribution limits than RRSPs (especially after age 40), they are less commonly used due to complexity, limited investment control, and ongoing costs. IPPs require actuarial and legal setup, and the investment decisions are usually managed by the investment company rather than the owner.

For most business owners, corporate-owned life insurance provides more flexibility, control, and strategic value than IPPs. However, IPPs may be appropriate in specific circumstances where the contribution advantage is significant and the complexity is acceptable.

For long-term capital that you don't need for operations, corporate-owned life insurance is the primary strategy for protecting it from tax. It provides tax-sheltered growth, estate liquidity, and CDA credits for tax-free distribution. The earlier you establish these policies, the more value they build and the more tax-efficient your estate extraction becomes.

PART VI: RETIREMENT, ESTATE, CONTINUITY

17. Retirement as Multi-Decade Wealth Transfer

For incorporated owners, retirement isn't a single event. It's a multi-decade process of transitioning wealth from your corporation to your personal accounts, and eventually to the next generation.

This requires thinking beyond traditional pension planning to coordinate corporate cash, personal investments, and insurance structures.

Retirement does not mean dismantling the HoldCo. It means changing its role, from accumulation engine to distribution coordinator. The HoldCo continues to compound wealth for generations while providing systematic, tax-efficient distributions for lifestyle needs.

The Dynasty-First Approach to Retirement

The "dynasty-first" approach means asking:

- How do we structure withdrawals to minimize lifetime tax?

- How do we maintain corporate wealth for estate strategies while funding personal lifestyle?

- How do we pass the business and accumulated wealth to the next generation efficiently?

Three Sources of Retirement Income

1. Corporate Cash and Investments

Your corporation may have accumulated cash and investments over decades. During retirement, you'll need to decide:

- When to withdraw: Timing matters for tax. Dividends, salary, and capital gains are taxed differently.

- How much to withdraw: Balance current lifestyle needs with future tax optimization and estate strategies goals.

- What to keep in the corporation: Some wealth may stay corporate for estate strategies, business succession, or future opportunities.

2. Personal Retirement Accounts

Personal accounts (RRSPs, TFSAs, non-registered) work alongside corporate wealth:

- RRSP withdrawals: Coordinate RRSP withdrawals with corporate dividends to optimize tax brackets

- TFSA flexibility: Tax-free withdrawals can supplement corporate dividends without increasing taxable income

- Non-registered accounts: Capital gains treatment may be more tax-efficient than dividend income in some situations

3. Insurance as Retirement Asset

Corporate-owned or personally-owned permanent life insurance can serve multiple retirement purposes:

- Tax-sheltered cash value accumulation

- Estate liquidity to pay taxes on corporate assets

- Tax-free death benefit for beneficiaries

- Potential source of tax-advantaged retirement income (policy loans, IRP strategies)

Designing a Withdrawal Sequence

Generally, you'll want to:

- Use TFSA withdrawals first: Tax-free, doesn't affect other income

- Consider tax-free policy loans: If you have corporate-owned permanent life insurance, policy loans against cash value are tax-free (they're loans, not distributions). This provides access to capital without triggering taxable events.

- Coordinate RRSP withdrawals with corporate dividends: Stay in optimal tax brackets

- Time corporate withdrawals strategically: Consider RDTOH, CDA, and capital gains treatment

- Consider preferred share redemption: If you completed an estate freeze, redemption of preferred shares can provide tax-efficient extraction. The tax treatment depends on the structure: amounts up to paid-up capital (PUC) are typically return of capital (tax-free), excess amounts may be treated as deemed dividends (eligible for dividend tax credit), and there may be capital gains implications depending on adjusted cost base. Work with your CPA to understand the specific tax treatment for your structure.

- Preserve some corporate wealth for estate strategies: If that's a goal

Example: Retirement Withdrawal Strategy

Scenario: Age 65, retiring with $2M in corporation, $500K in RRSP, $200K in TFSA, corporate-owned life insurance with $300K cash value, and preferred shares from estate freeze.

Years 65-70: Withdraw from TFSA first (tax-free). Consider tax-free policy loans from corporate-owned life insurance if needed. Take minimal corporate dividends to stay in lower tax bracket. Defer RRSP withdrawals. If preferred shares are available, consider strategic redemption (coordinate with CPA for tax treatment).

Years 70-75: Begin RRSP withdrawals, coordinate with corporate dividends to optimize tax brackets. Use CDA for tax-free corporate extractions when available. Continue using policy loans strategically if appropriate. Consider preferred share redemption as part of coordinated withdrawal strategy.

Years 75+: Continue coordinated withdrawals. Preserve some corporate wealth for estate if desired.

Note: This example is illustrative only. Actual withdrawal strategy depends on your specific circumstances, tax rates, goals, and the structure of your estate freeze and insurance policies. Policy loans reduce cash value and death benefit. Preferred share redemption tax treatment is complex and depends on paid-up capital, adjusted cost base, and other factors. Always work with your CPA and insurance advisor to model different scenarios and understand the tax implications.Retirement for incorporated owners is a multi-decade wealth transfer process. Coordinate corporate, personal, and insurance assets to minimize lifetime tax while funding lifestyle and preserving legacy. Work with your professional team to design and implement a withdrawal strategy.

18. Estate Strategies: Passing Wealth Forward

Estate planning for incorporated owners involves coordinating corporate structures, tax mechanisms, and legal tools to pass wealth efficiently to the next generation.

Estate planning represents the single most tax-efficient opportunity for extracting wealth from your corporation. While lifestyle extraction is necessary and taxable, extraction at death can be structured to minimize or eliminate tax entirely. The earlier you plan, the more effective the extraction strategy becomes. The higher you prioritize the importance of the estate transfer, the more wealth reaches the next generation.

This isn't about avoiding tax. It's about recognizing that death creates a unique tax event where the right structures can extract corporate wealth with maximum efficiency. Every year of delay is a year of lost opportunity for tax-efficient wealth transfer.

The Estate Strategies Challenge

When you die, your corporation faces several tax events:

- Deemed disposition: Corporate assets are deemed sold at fair market value

- Capital gains tax: Tax applies on the deemed capital gains

- Estate tax: Remaining corporate value may be subject to estate tax

- Probate: Corporate shares may go through probate

Each layer reduces what ultimately reaches your beneficiaries. The goal is to minimize total tax and facilitate efficient transfer.

Estate Strategies Tools

1. Estate Freeze

An estate freeze transfers future growth to the next generation while you retain current value. This can reduce the tax burden on your estate by shifting future capital gains to beneficiaries in lower tax brackets.

2. Trusts

Trusts can hold corporate shares and provide control while transferring economic benefit. They can also facilitate income splitting and tax optimization across family members.

3. Corporate-Owned Life Insurance: The Foundation of Efficient Estate Transfer

Life insurance is not optional for incorporated owners who want to pass wealth efficiently. It is the foundation of tax-efficient estate extraction.

Why Life Insurance is Essential:

- CDA Creation: Life insurance proceeds (net of adjusted cost base) create CDA credits, allowing tax-free distribution to beneficiaries. This is one of the most powerful tax-sheltering mechanisms available.

- Estate Liquidity: Corporate assets may trigger significant tax at death. Life insurance provides immediate liquidity to pay taxes without forcing asset sales or creating cash flow pressure.

- Tax-Sheltered Growth: Cash value grows tax-sheltered inside the policy, compounding without annual tax drag.

- Multi-Generational Impact: When structured properly, life insurance can fund estate obligations while preserving corporate assets for the next generation.

The Early Planning Advantage:

Life insurance requires time to build value and requires underwriting while you're healthy. A policy purchased at age 45 has 30+ years to build cash value and CDA credits. A policy purchased at age 65 has far less time to compound. The earlier you establish corporate-owned life insurance, the more tax-efficient your estate extraction becomes.

Corporate-owned permanent life insurance is not a "nice to have" for estate strategies. It is a must-have tool if you want to pass wealth efficiently to the next generation. Without it, your estate may face significant tax obligations that force asset sales or reduce what beneficiaries ultimately receive.

Think of corporate-owned life insurance as your estate's tax-efficient extraction engine. It provides liquidity when needed, creates CDA for tax-free distribution, and grows tax-sheltered over decades. The earlier it's established, the more powerful it becomes. This is why estate strategies cannot be deferred: the tools that create the most efficiency require time to build value.

4. Capital Dividend Account

The CDA allows tax-free distribution of corporate wealth to beneficiaries. Building CDA through capital gains and life insurance can significantly enhance estate outcomes.

Why Early Planning Matters

Estate planning efficiency compounds over time. The earlier you establish these structures, the more effective they become:

- Life Insurance: Requires time to build cash value and CDA credits. Underwriting is easier when you're younger and healthier. Premiums are lower when purchased earlier.

- Estate Freezes: Work best when implemented before significant growth occurs. The more value that accumulates before the freeze, the less is transferred tax-efficiently.

- Trust Structures: Require time to distribute income and optimize tax across family members. Earlier establishment allows more years of tax-efficient income splitting.

- CDA Building: Capital gains and insurance proceeds build CDA over time. The longer the planning horizon, the more CDA can be accumulated for tax-free distribution.

The Cost of Delay:

Every year of delay is a year of lost opportunity. A life insurance policy established at age 50 instead of age 45 loses five years of tax-sheltered growth and CDA building. An estate freeze implemented after significant corporate growth has already occurred transfers less value tax-efficiently. The structures that create the most efficiency require time to work.

Coordination is Critical

Estate planning requires coordination across multiple areas:

- Corporate structure: HoldCo/OpCo separation, share ownership

- Tax strategy: CDA, RDTOH, capital gains, dividend strategies

- Legal structures: Wills, trusts, shareholder agreements

- Insurance: Life insurance for liquidity and tax efficiency (essential, not optional)

- Business succession: Sale vs. family transfer

Estate planning is complex and highly personal. Tax rules, legal requirements, and family circumstances vary significantly. Always work with qualified professionals, your CPA, notary, and lawyer, to design and implement estate strategys. This guide provides general concepts only.

Example: The Cost of Delayed Estate Strategies

Scenario A: Early Planning (Age 45)

- Corporate-owned life insurance established: $2,000,000 death benefit

- 30 years of tax-sheltered cash value growth

- 30 years of CDA building through policy growth

- Estate freeze implemented before significant corporate growth

- Result: Maximum tax efficiency. Life insurance provides liquidity and CDA for tax-free distribution. Estate freeze transfers future growth tax-efficiently.

Scenario B: Delayed Planning (Age 65)

- Life insurance established: $2,000,000 death benefit

- 10 years of tax-sheltered growth (vs. 30 years)

- 10 years of CDA building (vs. 30 years)

- Estate freeze implemented after significant corporate growth has occurred

- Result: Reduced tax efficiency. Less time for structures to build value. More corporate growth already taxed at higher rates. Estate may face liquidity challenges.

The Difference: Early planning creates decades of tax-sheltered growth and CDA building. Delayed planning loses years of compounding and efficiency. The earlier you plan, the more wealth reaches the next generation.

Note: This example is illustrative only. Actual results depend on your specific circumstances, policy terms, corporate structure, and tax rates. Always work with your CPA, insurance advisor, and lawyer to design and implement estate strategys.Estate planning is the single most tax-efficient opportunity for extracting wealth from your corporation. The earlier you plan, the more effective these strategies become. Corporate-owned life insurance is not optional: it is a must-have tool for efficient estate transfer. Start early, coordinate with your professional team, and review regularly. The goal is efficient transfer of wealth to the next generation while minimizing tax and maintaining control where desired. Every year of delay is a year of lost opportunity for tax-efficient wealth transfer.

Review Structure

Take the first step. Begin your journey with a Structure & Strategy Review to identify gaps, optimize tax efficiency, and align your corporate investing with long-term goals.

PART VII: INTEGRATION & ACTION

19. The Dynasty Flow of Funds: Where the Next Dollar Goes

One of the most common questions we hear is: "I have $500,000 of surplus cash this year. Where should it go?"

Should it stay in the corporation? Go to an RRSP? Pay down the mortgage?

While every situation is unique, the math of tax efficiency creates a clear "Hierarchy of Savings." Think of this as a waterfall: you fill the first bucket until it overflows, then move to the next.

Level 1: The Foundation (Guaranteed Return)

- Target: Non-Deductible Personal Debt (Mortgage, Lines of Credit).

- Why: Paying this off offers a guaranteed, tax-free return that is hard to beat in the markets. It secures the family home and reduces monthly cash flow pressure.

- Action: Extract dividends to eliminate this debt first.

Level 2: The Tax-Free Zone (High Efficiency)

- Target: TFSA & RRSP (up to limits).

- Why: Tax-free (TFSA) or tax-deferred (RRSP) growth usually beats corporate investing because there is zero annual tax drag on the growth.

- Action: Maximize these accounts annually. They are your most efficient long-term compounding tools.

Level 3: The Accumulation Engine (High Volume)

- Target: Corporate Investments (Retained Earnings).

- Why: Once personal debt is gone and registered accounts are full, the Corporation is the superior wealth engine. It allows you to invest 100-cent dollars (pre-personal tax), creating a "Volume Advantage" that beats personal non-registered accounts.

- Action: Retain all remaining surplus here. Use "Tax-Smart" funds and Corporate Class structures to minimize passive income tax.

Level 4: The Tax-Sheltered Growth Vehicle (Corporate Life Insurance)

- Target: Universal Life or Whole Life Insurance with Deposit Options (Corporate-Owned).

- Why: Life insurance is the closest you can get to a TFSA in the corporation. Cash value grows tax-sheltered, and while there are insurance costs and deposit taxes to consider, these are often cheaper than paying tax on growth in traditional corporate investments. The tax-sheltered compounding can significantly outperform taxable corporate investments over the long term.

- Action: Consider allocating surplus to corporate-owned permanent life insurance (Universal Life or Whole Life with deposit options) for tax-sheltered growth. This is particularly valuable for long-term capital that you don't need immediate access to, and it builds CDA credits for future tax-free extraction.

Level 5: The Overflow (Lifestyle Liquidity)

- Target: Personal Non-Registered Accounts.

- Why: This is the least efficient bucket. You pay high tax to get the money out, and you pay tax again on the growth.

- Action: Use this only for short-term liquidity needs (e.g., funds needed for a renovation in 1-2 years) where accessibility trumps efficiency.

- If you owe the bank money personally: Pay it.

- If the government gives you tax-free room: Use it.

- For everything else: Keep it Corporate.

This hierarchy provides a clear framework for decision-making. Fill each level before moving to the next. This ensures your capital is working in the most tax-efficient environment available to you.

20. Coordination: Working With Your Professional Team

Corporate investing doesn't exist in isolation. It intersects with tax strategy, estate strategies, legal structures, and business operations. Effective coordination across these areas is essential for long-term success.

The Professional Team

Your team typically includes:

1. CPA (Chartered Professional Accountant)

Your CPA handles:

- Corporate tax strategy and compliance

- RDTOH, GRIP, and CDA calculations

- Passive income monitoring

- Dividend and extraction strategies

- Tax-efficient structure recommendations

2. Notary (Québec) or Lawyer (Ontario)

Your notary/lawyer handles:

- Estate planning structures

- Wills and trusts

- Corporate legal structures

- Shareholder agreements

- Business succession strategies

3. Insurance Advisor

Your insurance advisor handles:

- Life insurance needs analysis

- Policy structure and selection

- CDA planning with life insurance

- Estate liquidity planning

- Advanced strategies (IRP, IFA, Corporate Estate Bond)

4. Investment Advisor

Your investment advisor handles:

- Portfolio construction and management

- Asset location strategy

- Investment selection and monitoring

- Coordination with tax strategy

- Access to investment managers recognized for proven track records

How to Coordinate

1. Annual Strategic Review

Meet with your CPA annually (not just at tax time) to review:

- Passive income levels and projections

- RDTOH and GRIP balances

- CDA building opportunities

- Dividend and extraction strategies

- Tax law changes and implications

2. Integrated Planning

When making major decisions, involve relevant team members:

- Investment changes: Discuss with CPA for tax implications

- Estate planning: Coordinate CPA, lawyer, and insurance advisor

- Business succession: Involve lawyer, CPA, and insurance advisor

- Major withdrawals: Coordinate CPA and investment advisor

Effective coordination across your professional team is essential for long-term success. Corporate investing, and its tax optimization, estate strategies, and legal structures interact. Ensure these interactions are optimized through regular communication, integrated planning, and clear documentation.

21. Implementation Checklist & Next Steps

Understanding these concepts matters less than implementing them. This chapter provides a practical roadmap for getting started.

Phase 1: Assessment (Weeks 1-2)

Current State Assessment

Phase 2: Planning (Weeks 3-4)

Strategic Planning

Phase 3: Implementation (Months 2-3)

Implementation Steps

Phase 4: Ongoing Review (Annual)

Annual Review Process

Principles of Navigation

Principle 1: Adopt a Dynasty Mindset

True wealth is built over decades, not quarters. Shift from reactive annual filing to proactive multi-generational stewardship. This long-term lens changes every decision you make.

Principle 2: Compounding Is Holistic

It is not just money that compounds. We compound right thinking, actions, habits, and systems. These compound alongside tax savings to determine your family's ultimate outcomes.

Principle 3: Structure Precedes Strategy

Establish the right containers (HoldCo, Trusts, Accounts) before filling them. Structure determines what is possible; strategy just executes within those limits.

Principle 4: Plan Extraction Early

Do not wait until retirement or death. Systematic extraction strategies - for both lifestyle and estate - must start early to maximize efficiency and minimize the taxman's share.

Principle 5: Document to Teach

Documentation is not just for compliance; it is the primary tool for teaching the next generation. Use it to pass on intent, beliefs, values, rules, and purpose, ensuring the "why" survives alongside the "what."

Principle 6: Brand-Agnostic, Value-First Selection

Be brand agnostic. Select products, services, and managers solely based on their ability to deliver the best value that fits your long-term vision, not because of a label or sales pitch.

Next Steps: The Dynasty Implementation Plan

These concepts are general and educational. To move from education to action, follow this four-phase approach:

- Phase 1: Assessment. Clarify the purpose of your corporate capital (Retirement? Business buffer? Legacy?). Document where you are today.

- Phase 2: Planning. Work with your tax and legal advisors. Review your structure (especially before the 2026 rules settle in) and ensure your investment strategy aligns with your tax strategy.

- Phase 3: Implementation. Execute the changes. Establish your HoldCo, open the right accounts, and fund your insurance policies.

- Phase 4: Stewardship. Review annually. Document your decisions to teach the next generation.

Start with Phase 1: Assessment

You now understand the power of tax-optimized corporate investing. The difference between a standard approach and an integrated strategy can be meaningful over a single generation and more significant over multiple generations.

Begin your journey with a Structure & Strategy Review. This assessment will help you clarify the purpose of your corporate capital, document where you are today, and identify gaps, opportunities, and risks. You'll receive a confidential analysis to guide your next steps.

Together, we can position your corporation's wealth for the highest possible after-tax growth, not just for your lifetime, but for generations to come.

Final Thoughts

Each decision in this guide seems small. Separating your HoldCo. Choosing corporate class funds. Coordinating with your CPA. Defining the purpose for each dollar.

Individually, these are minor adjustments. Together, they compound.

Compounding works in both directions. Every dollar saved from unnecessary tax continues to grow. Every dollar lost to tax stops compounding immediately. Over twenty years, a 2% difference in after-tax returns can mean hundreds of thousands of dollars. Over thirty years, it can mean millions.

But compounding extends beyond money.

When you clarify purpose, you make better decisions. These decisions harden into habits, and those habits eventually define your outcomes.

When you coordinate with your CPA, you build systems. Systems build consistency, and consistency breeds confidence.

The steps in this guide are mechanical. They are small. But small changes, applied consistently over decades, multiply outcomes. The focus is installing the right systems so the right things happen consistently, year after year.

Information without action erodes identity. Alignment restores it. Understanding these concepts matters less than implementing them.

The cost of waiting is high. Every year that passes is another year of unnecessary tax drag and lost compounding, a permanent loss of potential wealth.

This content is for information and education only. It explains general concepts that may apply to incorporated business owners, but it is not personalized tax, legal, or investment advice.

Tax Considerations: Tax rules are complex and subject to change. Corporate tax treatment depends on your specific circumstances, province, and corporate structure. Always consult with a qualified CPA before implementing any tax strategy. Past tax treatment does not guarantee future treatment. Provincial variations in rates and rules may apply (Québec and Ontario have different tax rates and rules). The capital gains inclusion rate is 50% as of 2026. Tax policy can change over time, which is why building resilient, tax-efficient structures today is important regardless of the current rate.

Investment Considerations: Past performance does not guarantee future results. Investment values fluctuate and may lose value. Different investment structures have different risks, costs, and tax implications. Always review investment policy statements and understand fees and expenses. Corporate investing requires coordination with tax and estate strategies. Corporate Class funds, IPPs, and life insurance products have specific features, risks, and costs that must be understood before implementation. Borrowing to invest involves risk and requires careful analysis.

Regulatory Considerations: Mutual funds are distributed through WhiteHaven Securities Inc. Insurance products and related services are provided through iAssure Inc., an independent firm in the insurance of persons and in the group insurance of persons. These activities are neither the business nor the responsibility of WhiteHaven Securities Inc. Anton Ivanov is a Mutual Fund Dealing Representative with WhiteHaven Securities Inc. and a Financial Security Advisor (Québec).

Professional Coordination: This guide encourages coordination with your CPA, lawyer, and notary. Corporate investing should be integrated with tax strategy, estate strategies, and succession strategies. Every situation is unique, and what works for one corporation may not be appropriate for another. IPPs require actuarial and legal setup: consult with qualified professionals. Life insurance policies require underwriting and may not be available to all applicants. Advanced insurance strategies (IRP, IFA, Corporate Estate Bond) are complex and require careful structuring.

Our Role: We are investment and insurance professionals who collaborate with tax experts. We do not replace your CPA; we help you have better conversations with them. Our role is to coordinate investment and insurance strategies with your tax strategy, ensuring your professional team works together effectively.

No Guarantees: This guide does not guarantee any specific outcomes, returns, or tax savings. Structural improvements may not be appropriate for all corporations. Tax rules and rates are subject to change. Always seek professional advice before making decisions about your corporate investment structure.

Edition: 2026

Author: Anton Ivanov, iAssure Inc.